USD II: The Gasless Stablecoin for Gifting Crypto in 2026

Back to articles

Giving cryptocurrency like Ethereum or Bitcoin may sound simple, but in practice, it’s complicated.

You have to choose a secure crypto wallet, account for transaction fees, and make sure the recipient can access and safely store the crypto. There’s also the issue of price volatility—your gift could lose value before it’s even opened. For people new to the cryptocurrency market, that’s a steep learning curve.

This is why stablecoins—especially fiat-backed stablecoins like USD II—are changing how crypto gifting works.

What Are Stablecoins?

Stablecoins are a class of cryptocurrencies designed to maintain a consistent value, often pegged to fiat currency like the U.S. dollar. Their core benefit is price stability, which makes them ideal for everyday transactions, financial services, and gifting.

Unlike volatile cryptocurrencies such as Bitcoin, stablecoins serve as a reliable medium of exchange that avoids rapid price fluctuations.

Types of Stablecoins

These are pegged to traditional currencies and backed by reserves held by trusted custodians. They dominate the stablecoin market and are used for gifting, payments, and cross-border payment.

These use other crypto assets (like ETH) as collateral. They’re often overcollateralized to reduce volatility risks.

These are tied to physical assets like gold. Investors often use them to retain stability while diversifying into commodities.

These use smart contracts to expand or contract supply based on demand. However, as seen with TerraUSD’s collapse, algorithmic stablecoins can carry major potential risks.

These adjust value based on inflation or cost-of-living indexes instead of fiat. They help protect long-term purchasing power for crypto users.

Why USD II Is Perfect for Gifting

USD II is a fiat-backed stablecoin created by Burner and issued on the Base network. It’s backed 1:1 by U.S. dollars and treasury reserves, held by our financial partner, Bridge, and securely stored in a Privy-managed account.

Key Benefits of USD II:

- Gasless Gifting: Burner covers transaction fees on all USD II transfers through BurnerOS.

- Redeemable Anytime: Soon you will be able to redeem USD II for fiat dollars through Bridge (KYC required; fees may apply).

- Ready to Spend IRL: Soon you will be able to use USD II at Flexa-enabled merchants across the U.S.

- Secure by Design: Gifting happens through Burner wallet, a physical card using secure chips and a browser-based interface. No need to download apps or write down seed phrases.

Stablecoin Adoption Is Growing Fast

- Emerging Markets: In Latin America and Sub-Saharan Africa, stablecoins are helping people avoid inflation and use stable digital currency for international payments.

- Institutional Adoption: In the U.S. and EU, stablecoins are powering financial instruments, settlements, and business-to-business payments.

- Everyday Use: Stablecoins now account for over two-thirds of crypto transactions globally. Their role as a medium of exchange is replacing speculative use in favor of practical financial services.

Why Burner + USD II Are Better Together

Burner wallet makes gifting USD II fast and frictionless.

- No setup, no apps, no seed phrases

- Just tap the Burner card on a phone to access BurnerOS

- Gifting crypto becomes as easy as handing over a prepaid card but with the benefit of hardware security

- Burner supports stable digital assets, like USD II—ideal for consistent value delivery

Together, they solve key barriers around complexity, crypto taxes, and regulatory uncertainty—without exposing recipients to capital gains tax, capital loss, or taxable income surprises (though users should always consult a tax advisor).

Final Thoughts

Stablecoins like USD II are redefining how we think about gifting and transferring digital assets. With zero gas fees, built-in stability, and direct wallet access, USD II paired with Burner wallet makes crypto gifting feel more like sending a prepaid card—and less like configuring a blockchain. Ready to make your next crypto gift secure, stylish, and simple?

FAQ: USD II and Stablecoin Gifting in 2025

❓ What makes USD II different from other stablecoins?

USD II is gasless, redeemable, and integrated into the Burner wallet ecosystem. It’s optimized specifically for gifting, unlike more generic USD Coin or USDT implementations.

❓ Is USD II a fiat-backed stablecoin?

Yes. USD II is a fiat-collateralized stablecoin backed 1:1 by U.S. dollar and treasury reserves. It is considered part of the fiat-backed stablecoin class and can be redeemed for fiat currency.

❓ Is gifting USD II taxable?

In many jurisdictions like the U.S., gifting under the annual gift tax exclusion isn’t a taxable transaction, but recipients may face capital gains or taxable income obligations if they later convert or sell the asset. Always check with a tax advisor.

❓ What kind of wallet is Burner?

Burner is a physical card wallet that uses secure chips—similar to those in Ledger and Trezor—to provide advanced hardware-level security without complex setups or seed phrases. It pairs affordability and simplicity with a browser-based interface, making everyday Ethereum transactions easy, accessible, and secure.

❓ Can USD II be used for other purposes?

Yes. It works for everyday transactions, cross-border payment, saving, or as a digital representation of fiat currency. It’s versatile, secure, and easy to redeem.

❓ Who is Bridge?

Bridge is a financial technology platform that provides infrastructure for stablecoin issuance and management. It enables seamless conversion between fiat currencies and stablecoins, simplifying cross-border payments and digital asset management. Bridge is our financial partner holding USD II’s reserves and facilitating redemption into U.S. dollars.

❓ Who is Privy?

Privy is a secure user authentication and data management platform. It powers account creation and access for USD II by storing account data in encrypted, non-custodial containers.

❓ What is Flexa and how does it work?

Flexa is a digital payments network that allows merchants to accept crypto payments easily. Customers can spend cryptocurrencies, including stablecoins like USD II, at Flexa-enabled merchants. Flexa instantly converts crypto payments into the merchant’s local currency, simplifying transactions without additional complexity.

Get your Burner

What to read next

Back to articles

Who Is Satoshi Nakamoto? The Suspects and the 2026 Hunt to Unmask Bitcoin's Creator

More than 17 years after Bitcoin's first block, no one has proven who Satoshi Nakamoto is. We go through the leading suspects, the competing answers from a 2026 documentary and the New York Times, and what Satoshi's untouched coins say about holding bitcoin yourself.

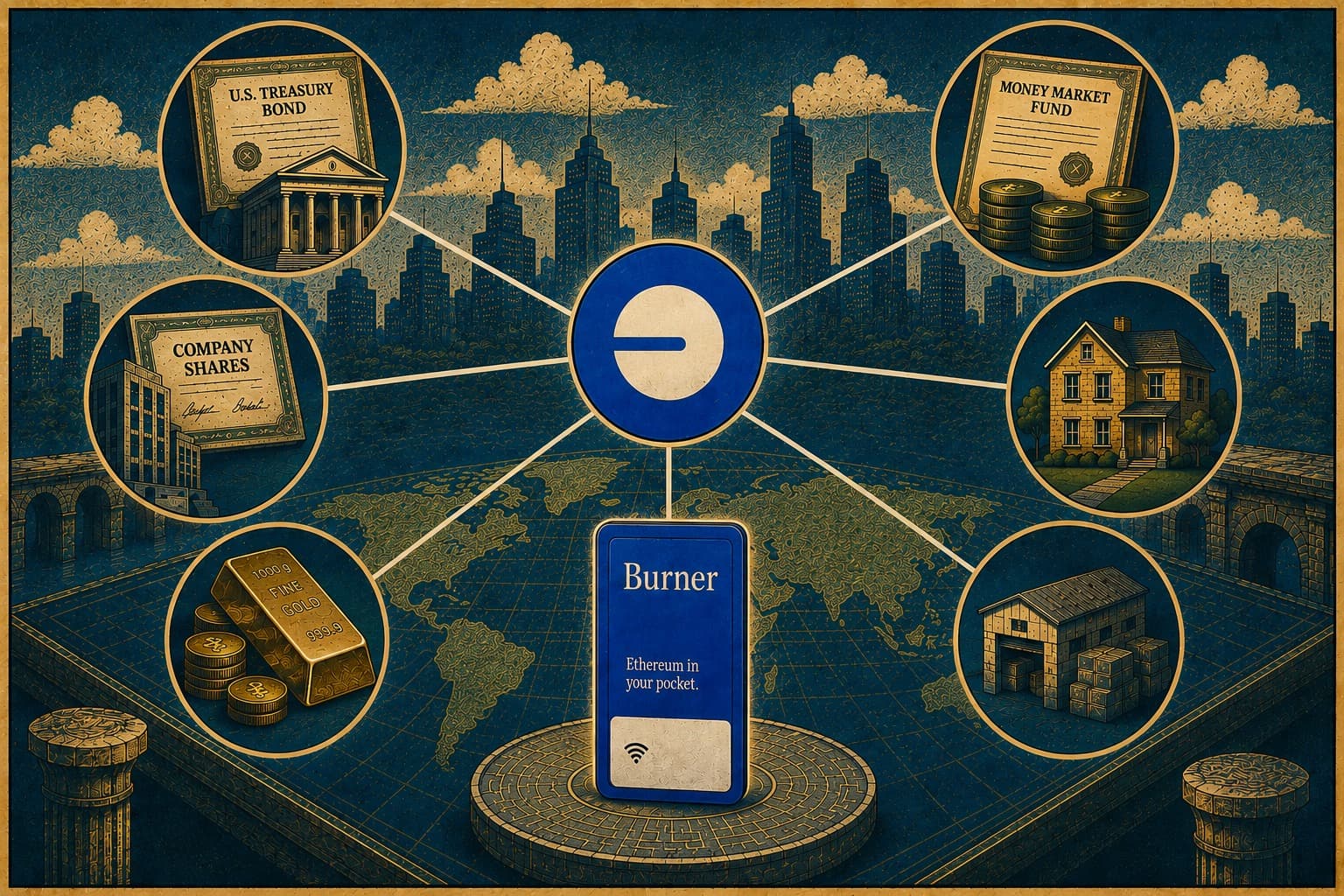

What is a Real-World Asset (RWA)? A Guide to RWAs on Base and How to Securely Store Them

A real-world asset is something that exists off the blockchain, like a US Treasury bond, a money market fund, a bar of gold, or a share of stock, represented on-chain as a token. The token isn’t a new asset with value of its own. It’s a claim on the real one, recorded on a blockchain so it can be moved, split, and held the way you’d hold any cryptocurrency.

Send Money Home Cheaper, Faster, and Easier by Mailing a Burner Card

Traditional remittance services charge an average of 6.49% per transfer, and the money can take days to arrive. Stablecoins move the same dollars for cents and settle in minutes, which is why even Western Union launched its own stablecoin in 2026. The work falls on the receiving end, where the recipient has to set up a crypto wallet before they can use the money. A preloaded Burner card takes that work off them. This post explains how stablecoin remittances work, why onboarding is the hard part, and how mailing a ready-to-use card moves the setup to the sender instead.