Join r/burnerwallet and Claim a Limited Edition Reddit Burner

Back to articles

Burner started with a simple goal: make self-custody and crypto gifting easier, safer, and more accessible for everyone. Whether you’re using Burner Ethereum to gift, store, and spend Ethereum tokens, stablecoins, and other digital assets, or Burner Bitcoin to gift, stack, and secure sats, the idea is the same: a low-cost, secure hardware wallet that works without apps, seed phrases, or prior crypto expertise.

Over the past year, we’ve connected with users everywhere — at events, on social, and in our Telegram community. The feedback and vibes have been incredible. Now, we’re making it even easier for Burner users and enthusiasts to connect with each other.

Welcome to r/burnerwallet

We’ve launched r/burnerwallet, a dedicated subreddit for the Burner community. It’s a place to:

- Share how you’re using Burner

- Get tips, answers, and advice from the Burner team and fellow users

- Keep up with updates, experiments, and new releases

Post and Get a Limited Edition Reddit Burner

To celebrate the launch, we’re giving away 100 limited-edition Reddit Burners to users who share their experience on r/burnerwallet.

Here’s how to claim yours:

- Own a Burner wallet: You’ll need your original order number from when you bought it.

- Post about your experience: Make a post on r/burnerwallet sharing your honest impressions.

- Fill out the claim form: Complete this form - include a link to your Reddit post, your email, and previous Burner order number.

Your feedback doesn’t have to be glowing to get a free Burner (but it’ll make our day if it is). We want to hear the good, the bad, and everything in between, because that’s what helps make the product better.

Short, low-effort posts (like “It’s awesome.” or "Let's go!") won’t qualify, so take a moment to share something thoughtful.

See You on Reddit

So, what are you waiting for? Head over to r/burnerwallet, make your first post, and secure one of the rarest Burners we’ve ever made.

Get your Burner

What to read next

Back to articles

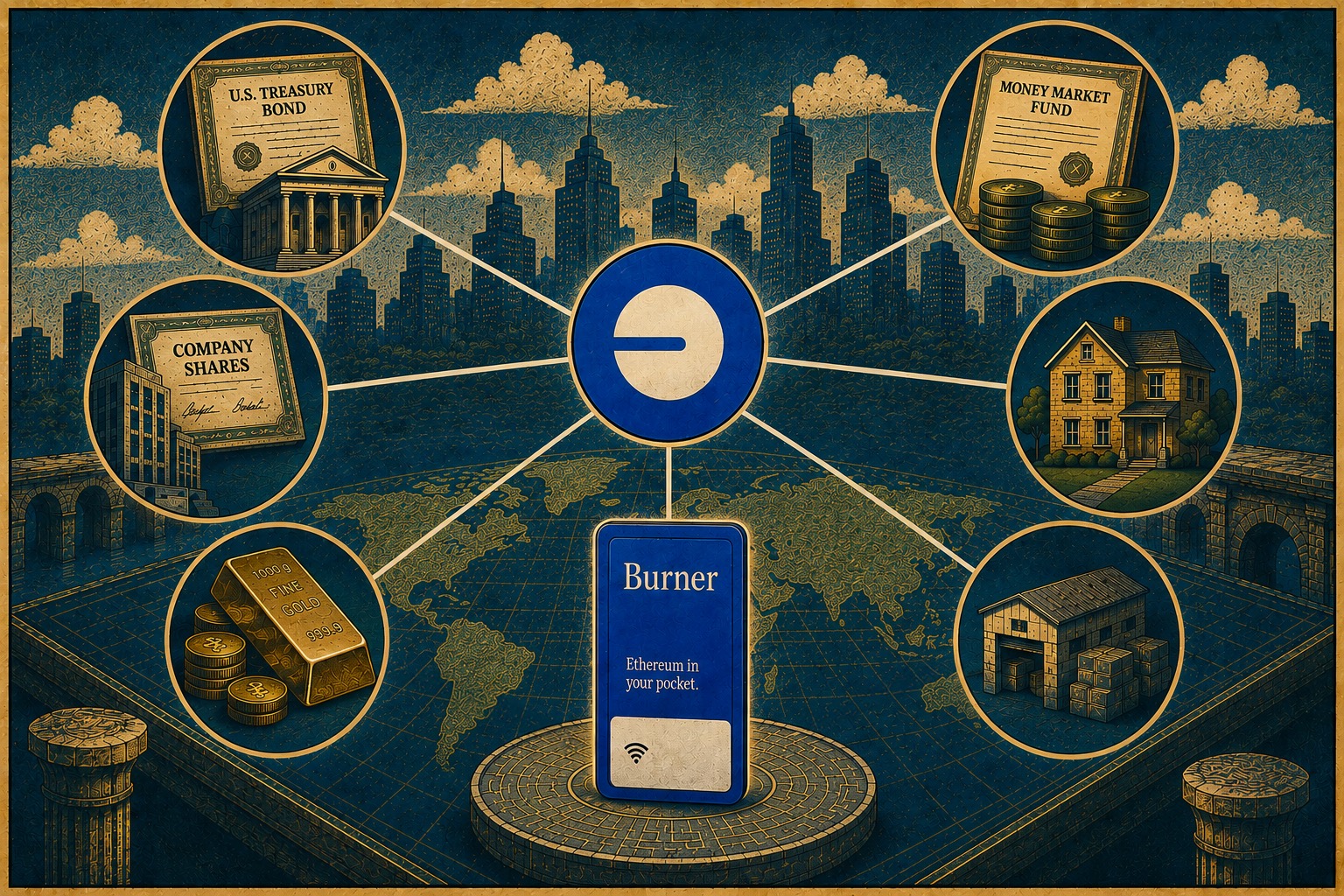

What is a Real-World Asset (RWA)? A Guide to RWAs on Base and How to Securely Store Them

A real-world asset is something that exists off the blockchain, like a US Treasury bond, a money market fund, a bar of gold, or a share of stock, represented on-chain as a token. The token isn’t a new asset with value of its own. It’s a claim on the real one, recorded on a blockchain so it can be moved, split, and held the way you’d hold any cryptocurrency.

Send Money Home Cheaper, Faster, and Easier by Mailing a Burner Card

Traditional remittance services charge an average of 6.49% per transfer, and the money can take days to arrive. Stablecoins move the same dollars for cents and settle in minutes, which is why even Western Union launched its own stablecoin in 2026. The work falls on the receiving end, where the recipient has to set up a crypto wallet before they can use the money. A preloaded Burner card takes that work off them. This post explains how stablecoin remittances work, why onboarding is the hard part, and how mailing a ready-to-use card moves the setup to the sender instead.

Payment Psychology That Makes Customers Spend More, And How You Can Copy It

Customers spend 64-177% more when the act of paying is separated from the act of buying. Disney, Starbucks, casinos, and cruise lines have all engineered their payment systems around that gap, while cash businesses sit at the opposite end, carrying the highest psychological friction of any payment method. This post breaks down the behavioral research behind the "pain of paying," explains why stored-value systems lower it, and shows how a Burner card loaded with stablecoins gives any small business access to the same spending psychology without building a proprietary platform.