The CLARITY Act Just Cleared the Senate. Here's What It Means If You Hold Stablecoins.

Back to articles

TL;DR

- The Senate Banking Committee advanced the CLARITY Act 15-9 on May 14, 2026. It's the closest a crypto market-structure bill has come to passing the Senate.

- The bill classifies Bitcoin (BTC) and Ether (ETH) as CFTC-overseen digital commodities, routes investment-contract assets to the SEC, and sends payment stablecoins to banking regulators.

- Section 605 protects your right to self-custody. Federal agencies can't ban or restrict a hardware wallet or software wallet used for lawful purposes.

- Stablecoin issuers still can't pay direct yield to holders, but exchanges can offer activity-based rewards tied to transactions, loyalty, or liquidity provision.

- The bill heads to the Senate floor next. It needs 60 votes to overcome a filibuster, and the White House is targeting a July 4 signing.

If you hold stablecoins or self-custody your crypto in a hardware wallet, you've been operating in a regulatory gray zone. U.S. crypto rules have come mostly from enforcement actions and conflicting regulator statements rather than a written rulebook. The CLARITY Act is the first federal attempt to change that. It's a market-structure bill that defines what each kind of digital asset is, assigns a regulator to it, and writes down protections for people who hold their own keys.

For anyone who holds Bitcoin or Ether, owns stablecoins, accepts them as payment, or keeps their keys in a hardware wallet, that makes it the first framework to map out how your activity actually gets regulated. After years of stalled attempts, it just took its biggest step yet in the Senate. Here's what the bill does, and where it stands.

Related: The SEC's DeFi Safe Harbor and What It Means for Self-Custody

What the CLARITY Act Actually Does

The bill sorts every digital asset into one of three categories and assigns each one a regulator:

Digital commodity. A token whose value comes from the use of the underlying blockchain, not from a central issuer. Bitcoin and Ether are the textbook examples. Both now sit explicitly under CFTC jurisdiction, ending a question the agency and the SEC have argued about in court for years. Most other layer-1 tokens on mature blockchains fall in here too.

Investment contract asset. A token sold as part of a fundraising arrangement that promised future returns from the work of an issuer. Examples include most early-stage token sales. The SEC takes the lead.

Permitted payment stablecoin. A digital dollar designed for payments, redeemable 1:1 for actual dollars, backed by reserves. Banking regulators (OCC, Fed, state banking agencies) take the lead, under the GENIUS Act.

The GENIUS Act, signed in 2025, set the federal rules for stablecoin issuers: 1:1 reserves, monthly disclosures, no direct yield. CLARITY extends that framework to the rest of crypto.

| Category | Regulator | Examples |

|---|---|---|

| Digital commodity | CFTC | Bitcoin (BTC), Ether (ETH), most layer-1 tokens on mature blockchains |

| Investment contract asset | SEC | Most early-stage token sales and fundraising offerings |

| Permitted payment stablecoin | OCC / Fed / State banking | USDC, USDT, USD II, other dollar-pegged payment tokens |

What Happened on May 14

On May 14, 2026, the Senate Banking Committee voted 15-9 to send the CLARITY Act to the Senate floor, the furthest a crypto market-structure bill has ever traveled in the upper chamber. The markup followed months of bipartisan negotiation and a last-minute compromise on stablecoin rewards, with two Democrats, Ruben Gallego of Arizona and Angela Alsobrooks of Maryland, crossing the aisle to advance it. The deal restricts crypto companies from paying savings-account-style interest on stablecoin holdings, while keeping a path for exchanges to offer activity-based rewards.

What happens next is a merger of the Senate Banking and Senate Agriculture versions of the bill. The combined bill then goes to the Senate floor, where it needs 60 senators to overcome a filibuster. The White House is targeting a signing ceremony around July 4.

What CLARITY Means for Stablecoin Holders

The CLARITY Act doesn't directly regulate people who hold USDC, USDT, USD II, or any other dollar-pegged token. It regulates the issuers, exchanges, and platforms you transact with. But three practical changes affect what your stablecoin balance can earn and how protected it is.

Direct yield from the issuer is off the table. Under the GENIUS Act passed in July 2025 and reinforced by CLARITY, stablecoin issuers can't pay interest, yield, or any savings-account-style return to holders just for holding the token. The banking lobby's argument is that paying yield turns stablecoins into a competitor for insured deposits without the same regulatory burdens. Circle, Tether, and Bridge can't cut you a check for sitting on USDC, USDT, or USD II.

Rewards from third parties are still allowed. The May 4 Senate compromise preserved an opening: exchanges and platforms can pay activity-based rewards tied to transactions, usage, loyalty programs, or liquidity provision. So while Circle can't pay you to hold USDC, an exchange can pay you for the volume you move through its rails. The banking lobby continues to oppose the carveout.

Reserves and disclosures get stricter. GENIUS already requires payment stablecoin issuers to keep reserves 1:1 in cash, short-term Treasuries, or central bank reserves, with monthly attestations and bank-level supervision. CLARITY adds consumer protection rules the states can also enforce. For holders, that means more public information about what's behind your dollar-peg, and faster enforcement when an issuer falls short.

What CLARITY Means for Bitcoin and Ether Holders

CLARITY isn't just a stablecoin bill. It's a market-structure bill, and the biggest market it draws lines around is Bitcoin (BTC) and Ether (ETH). For the first time, the federal government writes down what those two assets actually are: digital commodities under CFTC jurisdiction, not securities under the SEC's. That ends a question the agency and the industry have been litigating in court for years, and it shifts a few things in practice:

Spot Bitcoin and Ether trading sit on firmer ground. Bitcoin and Ether ETFs already trade in the U.S., but the underlying spot venues have operated in a registration limbo. CLARITY hands oversight of those venues to the CFTC with a defined registration path.

Ether's role as the rails for stablecoins gets recognized. If Bitcoin anchors crypto more broadly, Ether anchors stablecoins. Most U.S. dollar stablecoin volume actually settles on Ethereum or chains derived from it. Classifying Ether as a commodity and stablecoins as payment instruments puts the asset and the network it depends on on the same map, without routing either through securities law.

Self-custody applies the same way. Section 605's protections cover digital commodities too, not just stablecoins. The right to hold your own Bitcoin or Ether on a device you own is treated the same as the right to hold your own USDC.

Section 605 and the Right to Self-Custody

One provision that hasn't gotten the headline attention, but matters a lot if you run your own wallet, is Section 605.

"A United States individual shall retain the right to maintain a hardware wallet or software wallet for personal use."

Section 605 prohibits federal agencies from banning, restricting, or impairing an individual's ability to self-custody digital assets for lawful purposes. It covers both software wallets (browser extensions, mobile apps) and hardware wallets (physical devices that secure private keys). The Senate version preserves the same protection.

What Section 605 doesn't do: it doesn't override the Bank Secrecy Act, sanctions enforcement, anti-fraud actions, or other illicit-finance laws. If someone uses a self-custodial wallet to launder money or evade sanctions, that's still illegal. If you use it to hold your own savings or pay a contractor in stablecoins, federal agencies can't tell you you're not allowed to.

Compared with the European Union's MiCA framework, which restricts certain self-custody flows, CLARITY puts the U.S. in a more permissive position on hardware and software wallets.

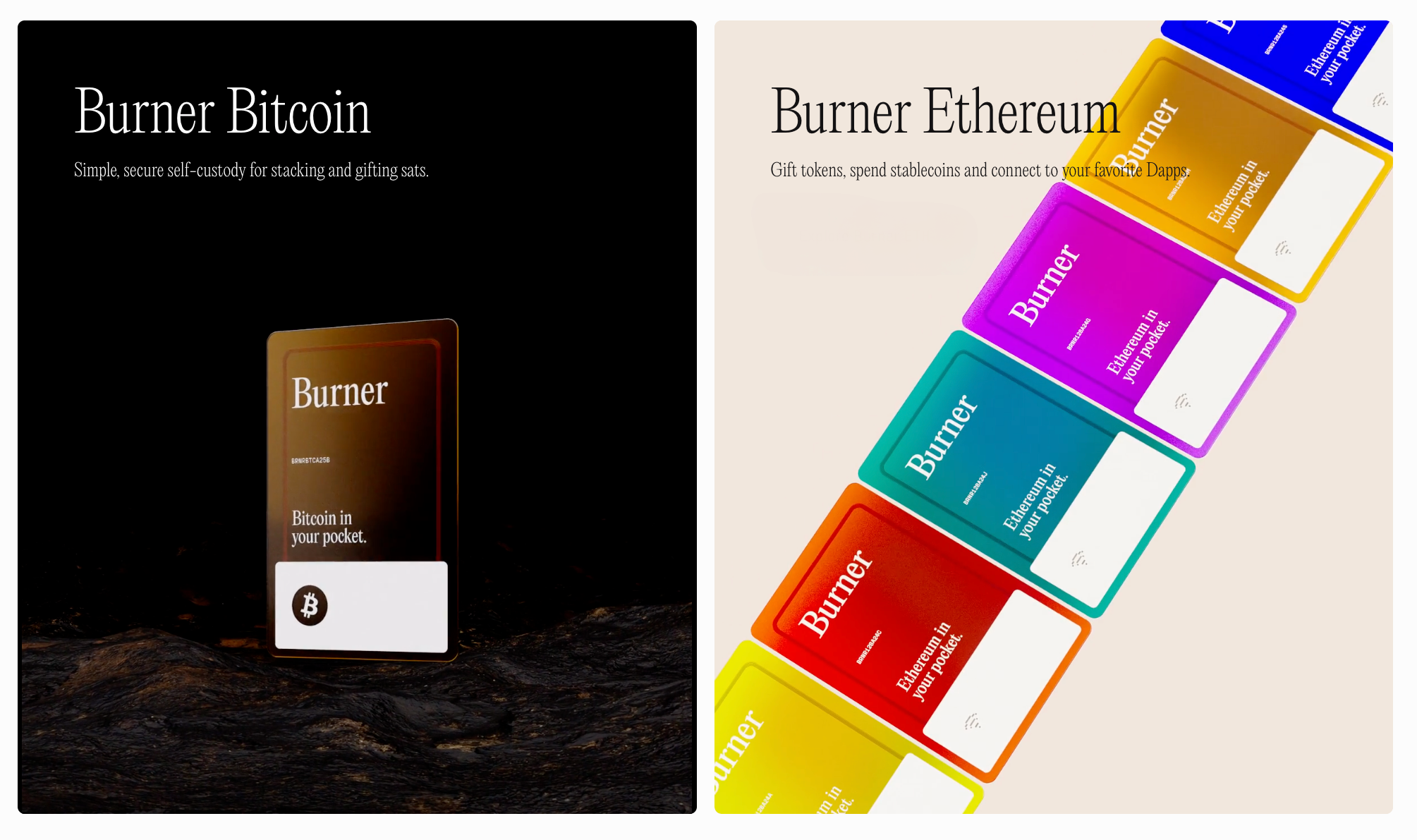

Burner is one such hardware wallet. It's an affordable, credit-card-sized device that uses the same secure-chip technology as more expensive wallets like Ledger and Trezor.

It comes in two versions: Burner Bitcoin and Burner Ethereum. In addition to holding ETH, Burner Ethereum can also store stablecoins like USDC and USDT. It features a non-extractable private key, no seed phrase to lose, and convenient PIN-based authentication. There's also no software to install. Just tap the card to your phone and your wallet opens in your browser.

What CLARITY Means for Stablecoin Payments

If the CLARITY Act passes as written, accepting stablecoins as payment moves from a legal gray area to a defined framework. The GENIUS Act governs the issuers, and CLARITY governs the rest of the stack.

For merchants, that's a meaningful change. Today, accepting stablecoins as payment means accepting some legal ambiguity about what your obligations are, what your customer's exchange is doing on the compliance side, and whether a future rule could pull the rug. Under the post-CLARITY framework, the answers are written down. Stablecoin issuers operate under banking-style supervision. Exchanges register with the CFTC or SEC depending on the activity. Payments using a permitted payment stablecoin sit inside the GENIUS framework.

And if you're a merchant who wants to accept stablecoins under that framework, that's what we built Burner Terminal for. It's a point-of-sale device designed for small businesses everywhere. It makes accepting stablecoins simple, secure, and free from chargebacks and high fees. Customers can tap any Burner card to pay with stablecoins, or use traditional payment networks Visa and Mastercard.

A new point of sale for stablecoin payments.

Final Thoughts

CLARITY hasn't passed yet, and the floor vote could still slip. Two fights are worth watching: Democrats want stricter ethics language barring senior officials from holding crypto business interests, and the banking lobby is still pushing back on the stablecoin-rewards carveout (a joint banking-industry letter to senators called it a "savings-account work-around").

The shape of the framework is already in the bill text. GENIUS sets the rules for stablecoin issuers, and CLARITY does the same for the rest of the digital asset stack. Section 605, separately, takes self-custody off the table for federal regulators, acknowledging that your right to hold your own keys already exists.

FAQ: The CLARITY Act

❓ When will the CLARITY Act become law?

The bill is on track for a Senate floor vote in late June or early July 2026, with the White House targeting a July 4 signing. To get there, the Senate Banking and Senate Agriculture versions have to merge, the combined bill needs 60 votes to overcome a filibuster, and the House has to reconcile any differences against its July 2025 version.

❓ Does the CLARITY Act ban stablecoin rewards?

It bans direct yield from the issuer. Under the GENIUS Act framework that CLARITY reinforces, a stablecoin issuer can't pay you interest just for holding the token. Activity-based rewards (transactions, loyalty programs, liquidity provision) from third parties like exchanges are still allowed under the May 4 Senate compromise.

❓ Are Bitcoin and Ether securities or commodities under the CLARITY Act?

Commodities. Both are explicitly classified as digital commodities under CFTC jurisdiction, not investment-contract assets under the SEC's. That settles a question the SEC and the crypto industry have been litigating in court for years, and it brings spot trading venues and self-custody for both assets under a written federal framework.

❓ Does the CLARITY Act affect my hardware wallet or self-custody?

It protects them. Section 605 prohibits federal agencies from banning or restricting an individual's ability to hold digital assets in a self-custody wallet, including a hardware wallet, for lawful purposes. The provision doesn't override the Bank Secrecy Act, sanctions, or anti-fraud enforcement, so existing illicit-finance rules still apply.

❓ What's the difference between the CLARITY Act and the GENIUS Act?

The GENIUS Act (signed July 2025) regulates stablecoin issuers: reserves, monthly disclosures, supervision by banking regulators, and the ban on direct yield. The CLARITY Act covers the rest of the digital asset stack: definitions, registration paths for exchanges, the SEC and CFTC jurisdictional split, self-custody protections, and a developer safe harbor. Together they form the U.S. crypto regulatory framework.

❓ Can the IRS still see my self-custody wallet under the CLARITY Act?

Section 605 protects your right to use a self-custody wallet, but it doesn't change tax reporting. The IRS already requires you to report gains and losses on digital asset dispositions, and that obligation continues. What CLARITY changes is the registration and licensing posture of platforms you transact with.

Get your Burner

What to read next

Back to articles

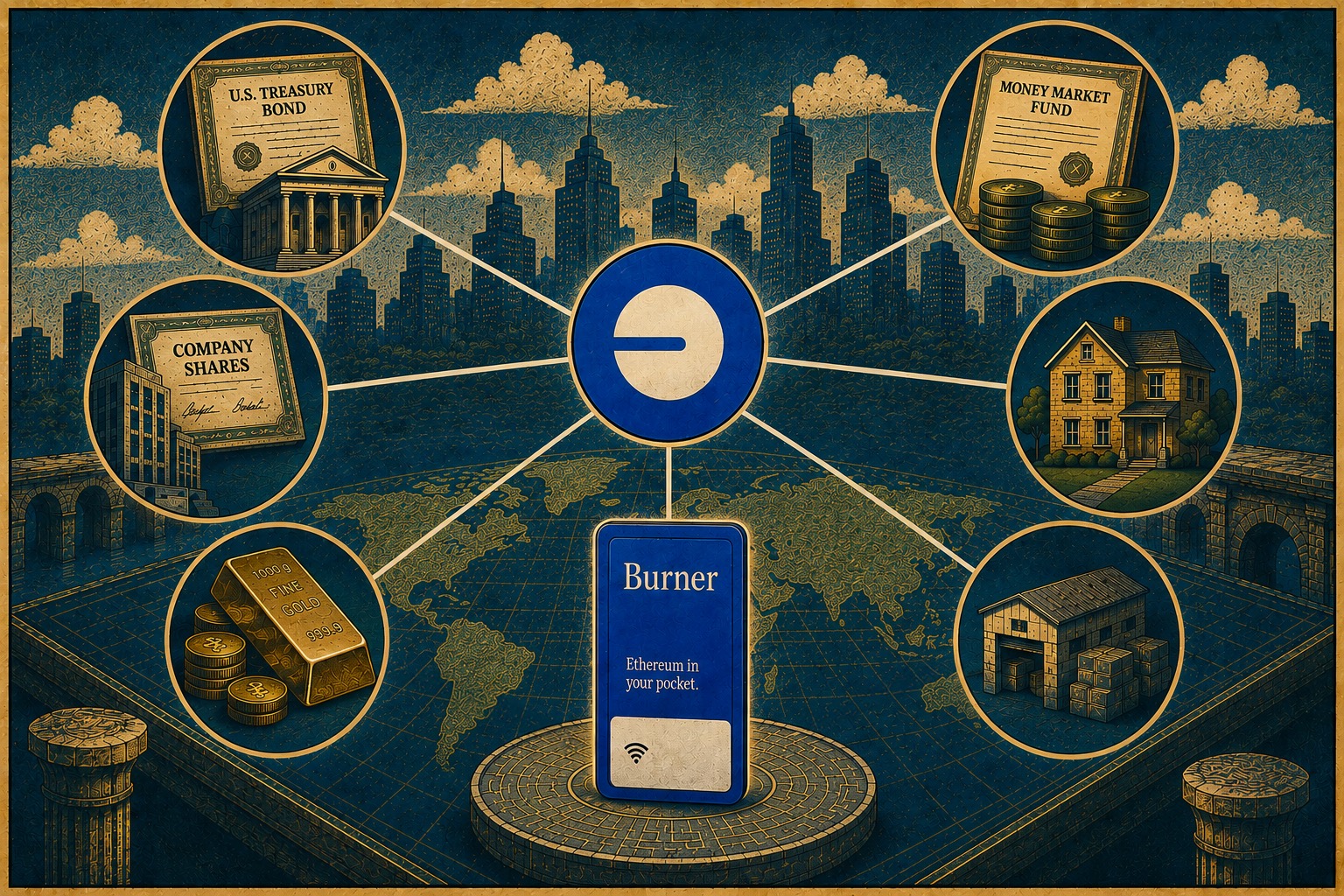

What is a Real-World Asset (RWA)? A Guide to RWAs on Base and How to Securely Store Them

A real-world asset is something that exists off the blockchain, like a US Treasury bond, a money market fund, a bar of gold, or a share of stock, represented on-chain as a token. The token isn’t a new asset with value of its own. It’s a claim on the real one, recorded on a blockchain so it can be moved, split, and held the way you’d hold any cryptocurrency.

Send Money Home Cheaper, Faster, and Easier by Mailing a Burner Card

Traditional remittance services charge an average of 6.49% per transfer, and the money can take days to arrive. Stablecoins move the same dollars for cents and settle in minutes, which is why even Western Union launched its own stablecoin in 2026. The work falls on the receiving end, where the recipient has to set up a crypto wallet before they can use the money. A preloaded Burner card takes that work off them. This post explains how stablecoin remittances work, why onboarding is the hard part, and how mailing a ready-to-use card moves the setup to the sender instead.

Payment Psychology That Makes Customers Spend More, And How You Can Copy It

Customers spend 64-177% more when the act of paying is separated from the act of buying. Disney, Starbucks, casinos, and cruise lines have all engineered their payment systems around that gap, while cash businesses sit at the opposite end, carrying the highest psychological friction of any payment method. This post breaks down the behavioral research behind the "pain of paying," explains why stored-value systems lower it, and shows how a Burner card loaded with stablecoins gives any small business access to the same spending psychology without building a proprietary platform.